|

At the Congressional hearings that followed, some critics even demanded that credit cards be outlawed.

Those banks that survived these early debacles began to find their footing in the 1970s. Technological innovations brought automation to their back rooms. Two competing umbrella associations, which would eventually become Visa and MasterCard, linked nationwide networks of merchants. Fraud was receding and banks were finally beginning to see profits after sending out more than 100 million credit cards. By 1978, the plastic revolution seemed like it was here to stay.

The reprieve would be brief.

By 1980 Citibank was being squeezed between New York state usury laws and double-digit inflation rates. "You are lending money at 12 percent and paying 20 percent," Mr. Wriston explained. "You don't have to be Einstein to realize you're out of business.''

The bank employed 3,000 people in its credit card unit in Long Island at the time, a fact that Mr. Wriston hoped would entice New York lawmakers to offer relief. "All you have to do is lift the usury ceiling to some reasonable amount and we'll stay here," Mr. Wriston recalled telling New York's political leaders. "And they said, 'Ah, ha! You really won't move. We're not going to do anything.'"

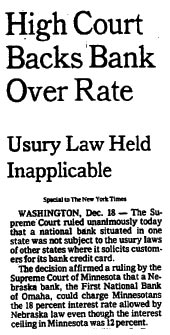

What allowed Wriston to make good on his threat to leave New York was a little-noticed December 1978 Supreme Court ruling. The Marquette Bank opinion permitted national banks to export interest rates on consumer loans from the state where credit decisions were made to borrowers nationwide.

So by early 1980, with New York refusing to go along, Citibank set out on a search for new place to base its credit card division. The pickings were slim. Usury laws were still on the books in the vast majority of the states. And federal banking rules required that before banks could set up operations outside their home state, a formal invitation had to be issued by the legislature of the state they wanted to enter. Local bankers had prevented any state legislature from ever extending such an invitation.

This was why Mr. Wriston was so eager to court Mr. Janklow.

In an effort to stimulate the local economy, South Dakota was in the midst of eliminating its usury laws. Mr. Wriston told Mr. Janklow that if South Dakota would quickly pass a bill inviting Citibank into the state, he would bring 400 jobs. To preempt concerns from local banks about new competition, Citibank also promised to open only "a limited" bank. "We'll put the facility in an inconvenient place for customers and we'll pay different interest rates," Mr. Wriston recalled telling Mr. Janklow. "All we want to do is use it to issue cards.''

For Mr. Janklow, it was an easy decision.

"To me, this wasn't a credit card deal, it was a jobs deal," he said. "It was an economic opportunity for the state. I was slowly bleeding to death."

With bipartisan support and backing from South Dakota's banking association, Janklow proposed a special "emergency'' bill. "Citibank actually drafted the legislation,'' he said. "Literally we introduced it, and it passed our legislature in one day.''

The arrangement ultimately brought 3,000 high-paying jobs to South Dakota and a host of new suitors from banks across the country. Citibank seemed to just be the beginning.

"It did fall out of the sky,'' Mr. Janklow said. "I was going to sleep at night thinking that we were the new financial center of America.''

But other states were quick to catch on. Delaware, which passed similar legislation the following year, would foil Mr. Janklow's dreams. "By that time, we'd captured a lot, but we thought we were going to get them all. Chase, Manufacturer's Hanover, Chemical -- they all went to Delaware. They were coming here," he said.

South Dakota would never become the next New York or Hong Kong, but Bill Janklow carved out a niche in credit card operations that remains one of the largest sources of jobs in the state. "The tragedy to me is that if Delaware would have waited one year," he said, "we would have had 20,000 more jobs in this state today."

The day Citibank first called will always remain bittersweet to Mr. Janklow. "Four different messages in one day from four different directions," he added. "That's never happened to me before or since."

The inflationary spiral that pushed Citibank to the precipice of disaster propelled the credit card industry into a decade of enormous profits. The elimination of usury restrictions paved the way for double-digit growth. Cardholders, it turned out, were willing to keep on paying 18 percent interest long after inflation subsided and the Federal Reserve lowered the interest rates it charged banks.

Between 1980 and 1990, the number of credit cards more than doubled, credit card spending increased more than five-fold and the average household credit card balance rose from $518 to nearly $2,700. With the cost of money sinking and average balances climbing, profits soared.

The industry also got an unintended boost from President Carter. In 1980, as part of a short-lived effort to tame inflation, the White House imposed a freeze on soliciting new credit card accounts. The freeze only lasted for a few months, but it was long enough for credit card companies to introduce a new concept -- the $20 annual fee -- without inciting mass defections.

Annual fees were a vital new source of revenues. But they also helped cover the costs for unprofitable "transactors'' -- those troublesome customers who avoided interest charges altogether by paying off their balances each month. Now even these customers were contributing to the bottom line.

But the flush times were about to face new perils. The first big sign of trouble came in 1990, when AT&T entered the market by offering a credit card with no annual fee. On the first day it was launched, the offer generated an astonishing 260,000 phone calls. Competitors panicked and quickly followed suit, spelling doom to the lucrative annual fees.

Then came what some bankers called "the Big Scare.''

It began on Nov. 12, 1991, at a $1,000-a-plate fundraising luncheon in New York for President Bush. At the last minute, an aide made a quick addition to a list of stimulus policies the president wanted to propose during his speech. "I'd frankly like to see credit cards rates down,'' he said. "I believe that would help stimulate the consumer and get consumer confidence moving again.''

Those two sentences had a powerful and immediate impact. As it happened, one of the luncheon guests was Alfonse M. D'Amato, then a senator from New York who had been critical of the 10-point gap between the prime rate and the interest rate typically charged to cardholders. The very next day, Sen. D'Amato proposed national legislation to cap credit card interest rates at 14 percent. After some 30 minutes of debate, the Senate voted 74-19 to approve the measure.

Panic swept through the banking industry. By Friday, economists were speculating about huge bank failures and the stock market plunged. The fervor for reform quickly cooled. In a television interview that weekend, Vice President Dan Quayle said if the proposed cap survived a House vote, it would likely be vetoed. By Monday, the tough talk about a national usury law became a call for a study of industry pricing practices.

Still, the industry was shaken. It was not just that the Big Scare signified an end to the comfortable and lucrative 10-point spread of the 1980s. It also marked a critical turning point in the broader evolution of the credit card -- from a mass-marketed, straightforward loan at 18 percent to a highly complex financial arrangement with ever-shifting terms and prices.

A key player in this evolution was Andrew S. Kahr, a child prodigy who earned his Ph.D. in mathematics from MIT by age 20. Now a financial industry consultant, Kahr pioneered several ground-breaking consumer banking products and founded a small credit card company in 1984 that would eventually become Providian, one of today's top 10 issuers.

Before many others in the industry, Kahr discovered that it was possible to analyze vast troves of consumer financial data and reliably predict which customers were least likely to pay off their credit card balances each month.

"It didn't require a lot of investigation to see that the people who paid in full every month were not profitable,'' Mr. Kahr said in a rare interview with FRONTLINE. Armed with exotic formulas and scoring systems, Mr. Kahr and his colleagues mined the data in relentless pursuit of the most lucrative "revolvers'' -- consumers who routinely carried high balances, but were unlikely to default.

"I don't believe in customer irrationality," Mr. Kahr said. "I don't find psychographics useful. I follow financial behavior."

Prospecting for profitable cardholders became an industry-wide preoccupation as growth slowed after 1990. Soon enough, the major credit card companies were using credit scores and other financial data to develop ever more sophisticated pricing and credit strategies. Instead of extending a generic credit line or charging a uniform rate, they set rates and limits based on computer-driven assessments of each consumer's risk of default. The higher the risk, the higher the rate.

"There was an opportunity to be more selective, both from the standpoint of credit quality and the standpoint of profitability and therefore to be able to offer attractive terms to the customers who we wanted," Mr. Kahr said.

One of the most attractive terms to customers and banks alike, according to Mr. Kahr, are higher credit lines. So in another innovation, Mr. Kahr saw that credit lines could be increased by slashing the required minimum payment. This increased revenue in two ways. First, since it would take longer to pay off balances, each dollar of principal would generate more interest income. Second, the principal itself would be increased because cardholders would be able to take on more debt while maintaining the same monthly payments.

With minimum payments cut from five percent to two percent, for example, a credit card company could increase a credit line to $5,000 from $2,000 and yet charge the same $100 minimum payment.

Today, two percent is the standard minimum payment, a practice that critics say obscures the true cost of debt and keeps consumers dangerously leveraged. Average household credit card debt, they point out, has nearly tripled since 1990 -- from about $2500 to $7500. Mr. Kahr, though, argued that "it is very consumer friendly" to allow people breathing room if they have a difficult month. "That's very important,'' he said, "because when people get behind on their payments, unfortunately, it becomes harder and harder to catch up."

Again and again in the face of crisis, the credit card industry has managed to outflank critics, sidestep legal hurdles and find new sources of revenue. Profits continue to break records, even in a market that has been deemed "mature" for over a decade. Now, some industry analysts believe, the industry's fabulous growth may be approaching a point of diminishing returns.

In recent years, however, the credit card industry has found -- and aggressively exploited -- yet another rich vein of profits: penalty fees.As with interest rates, an obscure ruling by the U.S. Supreme Court, this one in 1996, cleared the way for higher fees.

Duncan A. MacDonald, a former general counsel of Citibank's credit card division, spearheaded the case. "We were working this thing here for a good cause, free-market pricing,'' he said in an interview. "The late fees that were common across the industry, up until [the Supreme Court ruling], were in the $5 and the $10 range. And the economic thinking was that there had to be flexibility to allow up to $15.'' Instead, Mr. MacDonald said, the decision "took the lid off,'' as fees quickly shot up from $15 to $29 to as high as $39. "I certainly didn't imagine that someday we might've ended up creating Frankenstein,'' he said.

"It's been very dramatic,'' said Robert B. McKinley, founder and chairman of CardWeb and Ram Research, a payment card research firm. "A lot of banks didn't even charge an overlimit fee at that time."

Last year, penalty fees alone generated $12 billion in revenue. "Banks [are] raising interest rates, adding new fees, making the due date for your payment a holiday or a Sunday on the hopes that maybe you'll trip up and get a payment in late," said Mr. McKinley.

The new billions in revenue reflect an age-old habit of human behavior: Most people never anticipate they will pay late, so they do not shop around for better late fees. "Statistics show that most consumers are late some fraction of the time," Mr. Kahr said. "In the course of a year the average prime consumer will incur a late fee, the subprime consumer may incur two and a half late fees a year."

Today, behavior that violates the card agreement -- going over the limit or even a late payment with another creditor, for instance -- is used as an indicator of increased cardholder risk. The result is not just penalty fees, but also increases in interest rates. Some credit card customers complain bitterly about interest rates that suddenly shot up five-fold because of a single lapse.

"It's unfair," Mr. MacDonald said. "Millions and millions of people are being excessively charged late fees and bad-check fees and over-the-limit fees and then these 25 percent APRs to make the profits for the industry, so that they can keep the rates lower for people who are rate sensitive, who can in fact shop the system.''

Mr. Kahr, for one, makes no apologies. "If someone is riskier, he should be paying a higher rate,'' he said. "It's more economically sound. It's fairer for riskier people to pay a higher interest rate, higher fees, whatever it is, than less risky people.''

Ultimately, he argues, the market will decide what is fair.

"If there was a demand for a credit card product that never changed its terms and rates and stuck with the customer no matter what, I'd be running around telling people 'Let's market this wonderful fairness card,'" he said.

"You know -- 'transparency card,' 'rock solid card' -- whatever it may be. I don't believe that that would succeed."

|